Much attention has been paid and ink spilled on the issue of concentration risk as it relates to domestic equity benchmarks. Repetition aside, it’s a pertinent discussion.

Look at the topic through this lens. Investors devote capital to S&P 500 index funds and ETFs and comparable products thinking they’re getting broad market exposure. Yes, those funds hold a lot of stocks, but in cap-weighted form, they’re heavily concentrated in a small number of components. “Blame” the magnificent seven.

Just look at basic S&P 500 ETFs. As of July 30, the top four holdings in those funds commanded about a quarter of the ETFs’ weights. The top 10 holdings combine for more than 37%, meaning the other 493 components combine for less than 63% of these ETFs’ rosters. Translation: that’s a big a percentage directed to a small number stocks.

Add to that concentration risk isn’t confined to domestic equity indexes and the related funds. It’s creeping into global funds. Let’s examine that situation in more detail.

Magnificent 7 Effects Go Beyond the U.S.

Many market participants turn to global funds as best of both worlds alternatives meaning they like the mix of U. S. and foreign stocks under one umbrella, i. e. the aura of diversification. However, these funds aren’t as diverse as many investors believe.

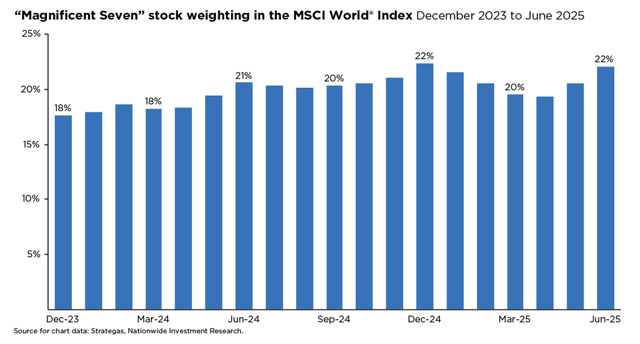

Take the case of the Vanguard Total World Stock ETF (VT), a highly popular fund as highlighted by its $48. 7 billion in assets under management. VT holds 9,914 stocks, implying its bets are spread geographically speaking, but the reality is North American equities represent nearly two-thirds of the portfolio. Nine of the ETF’s top 10 holdings, including all of the magnificent seven, are US-based firms. VT is just one example, but it confirms, as does the chart below, the dominance of the magnificent seven in global indexes.

(Chart Courtesy: Nationwide)

“This striking level of concentration within a supposedly diversified global benchmark highlights the growing dominance of U. S. mega-cap tech firms,” notes Nationwide’s Mark Hackett. “More importantly, it serves as a timely reminder: geographic diversification doesn’t always translate to true portfolio diversification. ”

Another way of looking at this scenario is remembering that weighting indexes and funds by market capitalization is said to be representative of market participants’ collective wisdom. That sentiment is accurate, but it’s also a reminder that wisdom doesn’t account for concentration risk.

Concentration Risk More Than Just U.S. Phenomenon

Nationwide’s Hackett rightly observes that concentration risk isn’t limited to U. S. indexes.

“International benchmarks are showing similar trends. In Germany’s DAX Index, for instance, the top ten constituents now represent over 60% of the Index’s total weight—a level of concentration that warrants close attention from investors,” he points out.

Another example from Europe: the top four holdings in the MSCI United Kingdom Index currently combine for more than 30% of that gauge. Point is investors looking to avoid concentration risk and allocate to truly broad funds need to perform some due diligence while not wagering that all markets outside the U. S. accomplish the aim of stock-level diversification.