The Invesco QQQ ETF (NASDAQ: QQQ) is higher by nearly 18% year-to-date, meaning 2025 will mark the six time in the past seven years that tech-heavy exchange traded fund finished higher on an annual basis with many of those yearly showings easily outpacing those of the S&P 500 and Russell 1000 indexes.

However, there’s a dark side to all that tech/artificial intelligence (AI) ebullience: It is sparking increasing talk of a bubble, including rampant comparisons to the dot-com bubble of 2000. Those comparisons are easy to make and simply because market participants are discussing a bubble, doesn’t mean one will come to fruition.

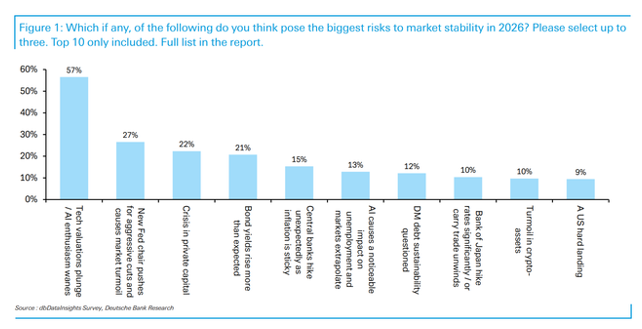

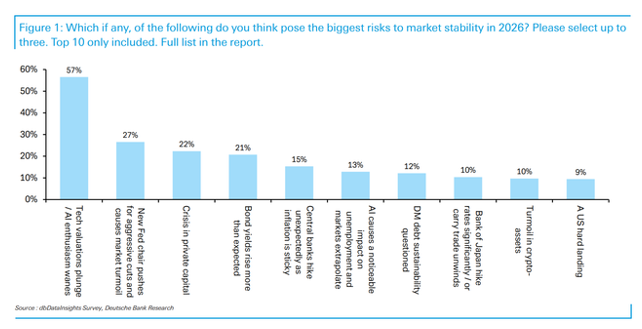

Still, and this is something for advisors to keep in mind in advance of 2026, the specter of a tech bubble is top-of-mind for investors. Deutsche Bank’s annual risk survey confirms the possible bursting of a tech bubble is the biggest concern for investors heading into next year.

(Image: Deutsche Bank)

Bubble Details Matter

Admittedly, I can’t say for certain, but it’s likely Deutsche Bank polled professional and institutional investors, not Main Street advised clients, but that doesn’t imply advisors should be dismissive of the date because their clients have also been hearing plenty about a tech bubble and they’re apt to share some of the concerns held by their professional peers.

With that in mind, it’s worth noting that the gap between AI/tech bubble worries and the next-largest concern is historically wide in the context of the Deutsche Bank survey. Said another way, investors are really, really concerned about that bubble and much less so about other issues.

“Unsurprisingly, a technology bubble bursting tops the ranking: 57% of respondents included it among their three biggest risks. We’ve never seen a single risk score so far ahead of the rest entering a new year, making it very clearly the dominant concern for 2026,” according to the bank.

Already enjoying resurgences this year, international stocks and funds could be avenues for defraying some of the tech bubble risk, because while AI is a global phenomenon, at the investment level, it’s heavily confined to the U. S.

“From memory, euphoria and bubble fears coexisted back then, though one key difference is that the late-1990s bubble was global, whereas any current potential excess looks far more concentrated in US AI-related stocks,” adds Deutsche Bank. “That said, today’s AI leaders are individually far larger — and more systemically important — than almost any stock was in 2000. So swings and roundabouts. ”

Remembering History

For better or worse, I’m old enough to remember the dot-com bubble bursting. In fact, my first job out of college was covering financial markets for a major news agency starting in 2000, so while I was young and inexperienced at that time, I do have some perspective.

One of the things that stuck with me, and probably a lot of folks involved with markets back then, was the foundation of hope and hype on which companies like eToys. com, Pets. com and others were built. Many of the dot-com era darlings didn’t survive not because their business ideas were bad – history has actually proven otherwise – but because they were financially flimsy, fundamentally flawed enterprises. Those traits fed the pricking of the bubble. Today’s AI giants are far more fundamentally sound and that cannot be overlooked.

“The leading cloud service providers (CSPs) are large, rational companies with strong balance sheets and positive free cash flow generation,” observed BNP Paribas. “To date, they have self-funded their AI capex primarily through operating cash flows. During the Internet and telecom bubble of the late 1990s, the companies bearing the brunt of the infrastructure investment were primarily [debt-funded. They] did not have stable cash-generating business segments to support them through the cycle. ”