It’s understandable that during strong-trending bull markets led by growth stocks investors embrace those vibes and perhaps even take it a step further, taking on thematic exposures.

The other side of that coin is that when growth stocks are in style, market participants often overlook the benefits of defensive exposure, forgetting the old sports adage about “defense winning championships. ” Advisors know better. They also know that there’s often more than meets the eye with equity investing, meaning there are occasions when what’s percolating below the surface underscores the need for defense.

The trick is convincing clients that reducing beta/volatility is a worthwhile pursuit. That’s no easy task coming off a lengthy span in which stocks with lower volatility lagged higher beta counterparts by wide margins. Interestingly, now may be an opportune time for advisors to discuss risk-reducing ideas with clients. Let’s explore why.

Contrarian Ideas

Undoubtedly, there are times when the “masses” get it right, but many a famed professional investor has extoled the virtues of contrarian perspectives. Data indicate that’s exactly what defensive equity investing is today: A contrarian strategy.

“The past 10 years, however, have seen lower beta stocks materially underperform the broader market. During that period, the S&P Low Volatility Index, which tracks the 100 least volatile companies in the S&P 500, gained just 9. 2%, compared to 14. 6% for the broader 500 Index,’ notes Vanguard. “That underperformance has caused investors to rush for the exits, pulling a cumulative $239 billion from defensive equity strategies since the end of 2022. ”

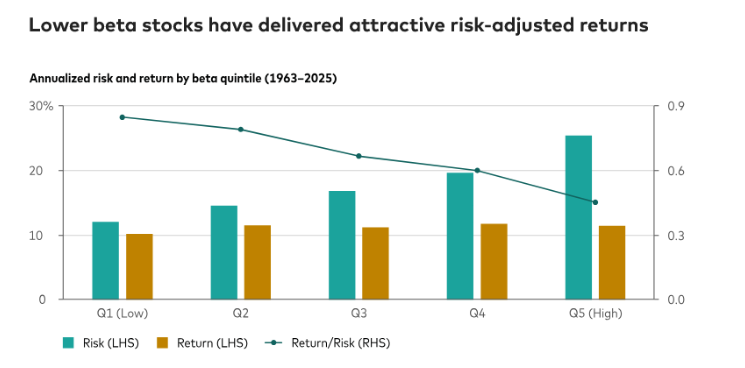

Something that many clients may not be aware of, particularly following the aforementioned stretch of high beta leadership, is that lower beta stocks actually deliver the superior long-term risk-adjusted returns as highlighted in the Vanguard chart below.

One takeaway from that and a point advisors should remind clients of is that when it comes to lower beta/volatility, it’s not so much about how those stocks or funds perform during bull markets. Rather, the benefits are accrued via those assets’ reduced downside capture during bear markets.

Defense Is Now Offering Value

Advisors also know that clients often conflate defensive sectors with value and while one can bear hallmarks of the other, these are two distinct factor concepts. They also know that that due to the advantages offered by defensive stocks, they often command premium valuations, indicating value isn’t always easy to come by.

That was certainly true in the years immediately following the global financial crisis when investors ditched low-yielding bonds in favor of defensive stocks. Fortunately for clients, today’s valuations on low beta equities aren’t demanding. That adds to the case for low beta conversations here and now.

“Under-allocating to defensive equities, especially at their current discount, could be like pulling your team’s starting defense to rest on the bench just as the game enters a critical phase,” concludes Vanguard. “While higher-volatility stocks have dominated in recent years, history shows leadership can revert when markets slow or stumble. And remember the unforgiving math of compounding: Losses weigh heavier than gains—a 50% decline requires a 100% rebound just to break even. ”