First, a bit of housekeeping. This article was written on Tuesday, Sept. 16 in advance of the Wednesday, Sept. 17 Federal Reserve meeting at which the central bank was widely expected to lower interest rates. Entering the meeting, it appeared highly likely the Fed would reduce borrowing costs, but this article was written without that certainty.

What is clear is that many equity investors believe lower rates are efficacious for stocks – wisdom that’s typically applied to bonds because bond prices and yields move inverse of each other. But as advisors know, there is a compelling case for equities during easing cycles. While the Fed hasn’t lowered rates this year, the S&P 500 is up 17% since September 2024 when the central bank lowered rates and did so again in November.

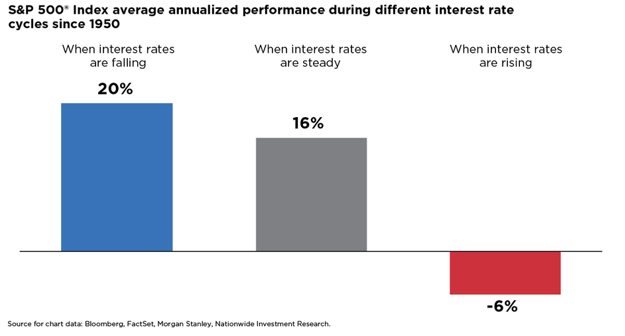

Additionally, history is on the side of equity investors following rate cuts and it’s expansive history at that. Going back to the 1950s, the S&P 500 usually responds favorably following dovish Fed action, as confirmed in the chart below.

(Image: Nationwide)

It’s not unreasonable to expect the newest Fed easing campaign will bring more the same on the basis that there’s “pent up” demand for lower rates and a case for such action because the jobs market is clearly weak.

Why Rate Cuts Matter

For some market participants, simply knowing that lower rates are here is enough, but more experienced investors know it’s worth examining why this scenario can be supportive of equity upside.

“They reduce borrowing costs for companies, which can boost profitability and spur investment. Rate cuts also support valuations, as lower yields make equities more attractive relative to bonds and help justify higher multiples,” notes Mark Hackett of Nationwide. “Historically, earnings have risen modestly during rate-cutting cycles that weren’t tied to recessions—such as in the mid-1980s and mid-1990s. Yet equity markets surged during those periods. ”

There are also sector-level implications derived from Fed easing/tightening. Said another way, some sectors are more rate-sensitive than others and if the Fed obligates, some value-oriented groups could challenge mega-cap growth for the domestic equity performance crown.

“Typically, economically sensitive sectors lead during easing cycles—think financials, industrials, consumer discretionary, and small caps,” adds Hackett. “Given the performance and valuation gap between large-cap tech and these cyclical sectors, the latter have shown relative strength in recent months. If expectations for Fed rate cuts continue to build, these stocks may have room to run. ”

Proper Positioning Matters

Beyond stocks and bonds, other assets stand to benefit from lower rates, including gold and perhaps bitcoin. Both are already high fliers this year and have spent considerable time flirting with record highs, but lower bond yields could make bitcoin and bullion more appealing.

How advisors and investors opt to play lower rates is obviously meaningful, but that sentiment is amplified because the September rate cut (assuming it was delivered) is unlikely to be a one-off. Goldman Sachs recently forecast three rate reductions, including September, into year-end and two more next year. If that outlook is accurate, stocks and other risk assets could have long runways for more upside.