It was just two to three years ago that cash was a rewarding asset class. An unprecedented inflation spike forced the Federal Reserve to take interest rates to the highest levels in more than two decades, slamming bonds in the process while making cash look like the bell of the ball.

These days, the national average on a high-yield savings account (HYSA) resides around 4. 60% APY, which is better than plenty of bond funds, and some banks are offering 5%. That’s pretty good for a supposedly risk-free investment. Of course the rub is that those rates will come down when the Federal Reserve cuts borrowing costs, a scenario that could materialize as soon as next month.

Even if the Fed speeds along rate cuts, that would likely be in an effort to prop up a softening U. S. economy. In such a scenario, it’d be reasonable to expect many skittish investors to remain in cash of their own volition and for advisors to increase cash holdings within client portfolios in an effort to mitigate risk.

Still, that doesn’t imply that cash is totally bereft of risk. Cash is like any other asset class in that investors need to get the allocation size within their portfolios. Too much cash and a portfolio likely misses out some upside when risk assets are in style. Too little and the portfolio isn’t adequately prepared for times like 2022.

Answering Cash Riddles

Cash shares something else in common with asset classes: the percentages it should command in portfolios depend on other factors, including an investor’s age, objectives and risk tolerance.

“A general rule of thumb is that cash or cash equivalents should range from 2% to 10% of your portfolio, although this will vary from person to person,” according to U. S. Bank Wealth Management.

It’s safe to say that a Gen Zer or a millennial can be in the 2% to 3% cash camp while baby boomers ought to be at the higher end of that range. However, there are caveats. For example, a more youthful market participant may want to hold higher levels of cash if they’re saving for a home. Smart move, but it’s not etched in stone because when rates are low, their cash rewards dwindle while their mortgage rates turn favorable.

“One situation where setting aside extra cash may make sense is if you’re planning on a big purchase or expense within the next few years, such as buying a home, undergoing a major home renovation or paying for college tuition,” adds U. S. Bank. “On the other hand, you may want to maintain a lower cash position based on your ability to meet short-term cash needs through borrowing. In a low-interest rate environment, for example, you might be able to tap into a home equity loan or line of credit. It avoids the need to set aside extra cash. ”

Another Cash Question

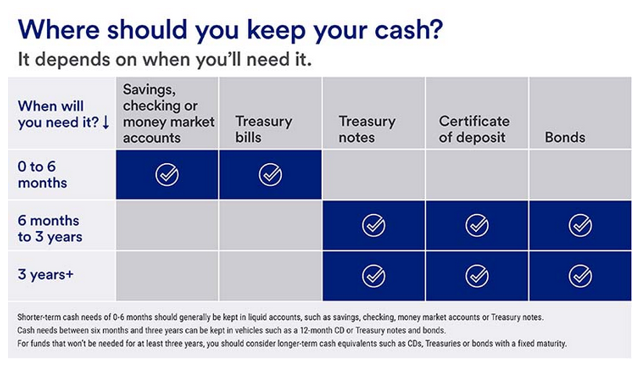

Without the guidance of an advisor, many investors that want to hold cash simply gravitate to savings accounts with attractive interest rates and leave at that. There’s a more strategic way of doing things and it can potentially enhance the rewards associated with holding. Check out the U. S. Bank table below for tips on being smart with cash.

“You should assess the percentage of cash and cash equivalents in your investment portfolio at least annually, tied to your regular financial plan review,” concludes the bank. “It’s the most effective way to assure that your portfolio is positioned in a way that will help you achieve your financial goals. ”