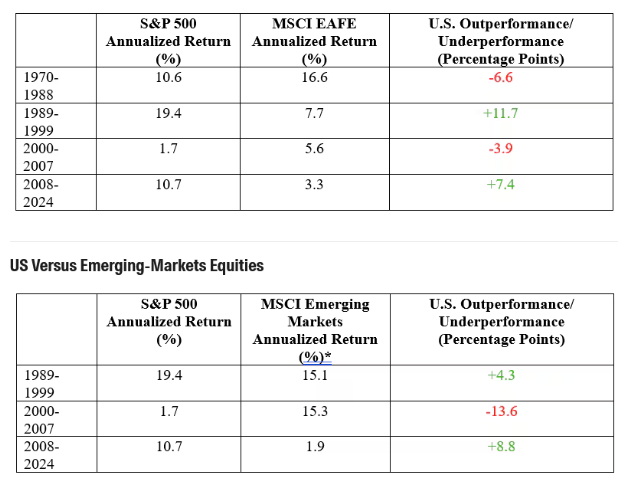

For the 10 years ending June 25, the MSCI ACWI ex USA IMI Index returned 77. 2%, or less than a third of the 243. 5% returned by the S&P 500 over the same period. From 2019 through 2024, 2022 was the only year in which the MSCI ACWI ex USA IMI Index “beat” domestic stocks and that was a case of performing less poorly, than beating the S&P 500 to the upside.

In other words, it’s understandable that investors largely glossed over international equities because for a decade-plus, the rewards simply didn’t justify the risk. That scenario is changing in 2025 as highlighted by a year-to-date gain of 16. 7% for the MSCI ACWI ex USA IMI Index while the S&P 500 is up just 4. 2%.

After years of hearing about the benefits of diversification vis a vis ex-US stocks and the low valuations found within the asset class, investors’ faith is finally being rewarded. Importantly, some experts believe international stocks’ impressive start to 2025 is a sign of things to come and this could be the dawn of a new era in which ex-US equities beat domestic counterparts. That would be something because over the past five decades, there haven’t been many extended periods in which international beat U. S.

(Tables Courtesy: Morningstar)

Smart Money Says Bet on International Stocks

For those that like to follow the so-called smart money, that crowed is bullish on ex-US stocks and they’re wagering on a multi-year period in which that asset class will beat U. S. equities, helped in part by the declining dollar.

“Consistent with the dollar bearishness, a majority of respondents expect international stocks to be the best performing asset over the next 5 years,” notes Candace Browning, head of research at Bank of America. “Investors today have the largest overweight in Eurozone and emerging market (EM) stocks and the largest underweight in the U. S. ”

Investors are now constructive enough on ex-US stocks that one of the oft-mentioned contrarian trade ideas being bandied about by professional is long domestic/short European stocks, according to Browning. It’s also widely noted that being short the U. S. dollar is one of the world’s most crowded trades at the moment. That doesn’t mean the greenback is due for an imminent rebound. It could be mired in a slump for some time, further boosting the case for international shares.

“From our vantage point, if the dollar starts on a new bear cycle, overseas assets will start to look more appealing for U. S. investors,” notes RBC Wealth Management. “And investors outside of the U. S. will no longer have the benefit of a strong dollar acting as a tailwind to the returns of their U. S. assets. This will likely result in further rebalancing away from the U. S. as the dollar declines, and foreign investors’ sales of U. S. assets will weaken the dollar further in a gradual feedback loop. ”

Dollar Declines Matter

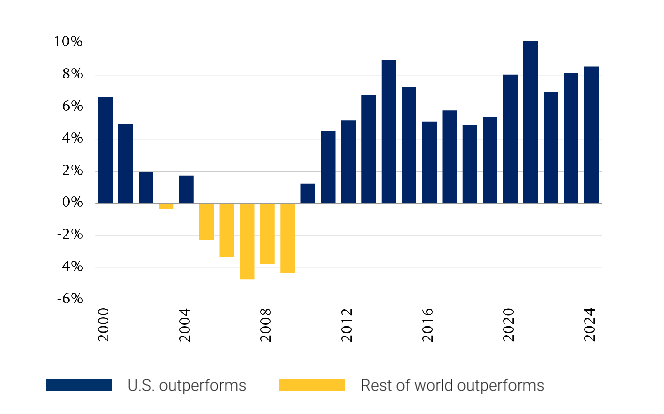

Yes, there are avenues for winning with international stocks when the dollar is strong, primarily currency hedged exchange traded funds. However, history confirms that the periods of true international out-performance usually coincide with dollar weakness.

(Chart Courtesy: RBC Wealth Management)

“If the dollar cycle switches to a bear market similar to the 1999–2009 period, we believe international investors’ appetite for non-U. S. stocks will resurface, as the MSCI All Country World Index beat the S&P 500 in seven out of those 11 years,” notes the asset manager.

Translation: investors betting on international stocks are wagering against the dollar. Given the federal government’s inability to reduce spending, that’s a bet that could pay off.