Optimal Roth Conversion Is a Highly Complex, Non-Linear Math Problem. Neither Wall Street Nor AI Gets It Right

Roth conversions refer to withdrawing money from a tax-deferred retirement account, typically a regular IRA or regular 401(k), and transferring the funds to a Roth IRA or Roth 401(k). You need to pay taxes on the amount withdrawn in the year of conversion. But your future Roth withdrawals, whether of income or principal, are tax-free. Plus, Roth withdrawals don’t count as MAGI — Modified Adjusted Gross Income. Hence, they neither kick up the taxation of your Social Security benefits nor raise your Medicare Part B and D IRMAA premia taxes.

Depending on their size, the immediate tax hit from Roth conversions can be nasty. But the reduction in future taxes can more than offset the short-term tax increase. This NY Times article on MaxiFi® Planner’s Roth Conversion Optimizer™ explains why “Go Big or Go Home” — doing most or all of your Roth conversions in the near term, even if doing so moves you into the top nominal federal tax bracket, generally results in the lowest lifetime taxes (the present value of current plus future taxes).

New to my Substack? MaxiFi® refers to my company’s economics-based financial planning software. These posts demo MaxiFi® Roth Conversion Optimizer™ including its ability to a) determine your estate-maximizing Roth conversion plan and b) use additional regular IRA/401(k) withdrawals to cover taxes on conversions and, thereby, avoid a cash-flow crunch.

Why Finding the Optimal Roth Conversion Plan is So Complex

There are seven different lifetime tax reductions arising from Roth conversions. First, there’s the exemption of Roth withdrawals from federal income taxes. Second, Roth withdrawals don’t trigger higher taxation of your Social Security benefits. Third, Roth withdrawals don’t trigger higher Medicare Part B and Part D IRMAA premiums. Fourth, Roth withdrawals aren’t subject to state income taxation. Fifth, Roth withdrawals don’t trigger higher state taxation of your Social Security benefits in states that tax such benefits. Sixth, paying, in the short run, higher taxes out of your regular assets means lower future taxable regular asset income and, therefore, lower taxation of that income. Seventh, lower future taxable regular asset income also means lower future state income taxes.

Figuring out precisely how much to convert each year to minimize your lifetime taxes is a problem with an infinite number of possible solutions. Say you’re 50 and can live to 100. Then you have 50 years left during each of which you can convert whatever you’d like, provided you have tax-deferred assets left to convert.

Moreover, the longer you wait to convert, the more you’ll have to convert as you earn income on your remaining regular IRA, 401(k), or other tax-deferred retirement accounts. In addition, as you keep working, you may continue to contribute to tax-deferred retirement accounts. Doing so means even more tax-deferred assets available, over time, for conversion.

Roth Conversions Involve Chickens and Eggs

The problem I’ve described is already extremely tough given its multiple moving parts and the fact that conversions in one year impact the gains from conversions in all other years. But the problem is actually much tougher.

Thus, smack dab in the middle of the already immensely complex Roth optimal conversion calculation is a huge “Which came first?” chicken and egg problem. Optimal conversions impact taxes, which impact spending, asset accumulation, and asset income, which impact taxes, which impact optimal conversions, which impact … . MaxiFi solves this massive simultaneous equation problem in seconds producing internally consistent, immediately verifiable results.

Want to check that MaxiFi’s Roth conversion optimizer delivers your highest lifetime tax savings? Simply modify its optimal conversion strategy in a different profile and run a comparison of the two. You’ll immediately see that the optimal strategy delivers lower lifetime taxes and either higher lifetime spending or a higher terminal estate depending on what you choose to optimize.

How Conventional Planning Avoids the Tough Roth Conversion Math

Wall Street’s conventional planning methodology was primarily developed for one purpose — to gather AUM — assets under management. The more AUM, the more fees Wall Street can charge. If conventional planning bore even a remote connection to economics-based planning, it might at least point you in the right direction. It doesn’t. And if its investment advice systematically beat the market, the fees might pay for themselves. They don’t. As described here, the vast majority of Wall Street stock-fund managers underperform the market. Yet these money managers have no compunction charging you for their professed expertise.

Conventional planning is also designed to avoid the just-mentioned simultaneity problem. Clients are forced to set and forget their retirement spending target. This makes no sense for the vast majority of us who wish to spend our tax savings from Roth conversions rather than add them to our adviser’s AUM.

Finally, in ignoring pre-retirement spending, conventional planning avoids the major cash flow constraints facing working households — constraints that MaxiFi fully handles and which critically impact how much and when to convert.

Wall St./AI Off-Base Conversion Method — Fill Up Federal Tax Brackets

Wall Street’s “solution” to Roth conversions is to fill up your federal tax bracket. Specifically, conversions are recommended in years when federal tax brackets and their associated nominal tax rates — reported in the IRS’ 1040 tax tables — are low compared to future tax brackets. The idea is to convert as much as possible in low federal-income bracket years, but not enough to push yourself into a higher federal-income tax bracket in those years. This is called filling up your tax bracket.

MaxiFi gives you the option to Roth convert using this approach. We do so to show you what you’ll lose following this strategy. Indeed, MaxiFi goes one step further. It restricts filling up federal tax brackets to years when your bracket is below average. Finally, for those concerned about losing Obamacare subsidies, it lets you restrict conversions to keep your AGI (adjusted gross income) below your desired maximum.

Federal Tax Brackets Don’t Reference Total Effective Tax Rates

Federal bracket tables don’t incorporate Social Security benefit taxation, IRMAA taxes, or state-income taxes. Consequently, you may think you’re in, say, a 24 percent marginal tax bracket when your true (effective) bracket is dramatically higher. Social Security benefit taxation can, by itself, raise your effective marginal tax rate above 50 percent. Add in Medicare Part B and D IRMAA taxes and we’re taking effective tax rates that can be crazy high.

Here’s the IRMAA story: Once you reach age 63, extra income means higher IRMAA taxes two years from now, assuming you enroll in Medicare at 65. But the IRMAA tax is like no other. Consider a couple on Medicare or one that will be on Medicare two years hence. If the couple’s current-year MAGI puts them just below the highest IRMAA tax bracket threshold that will prevail in two years, an extra dollar of taxable income this year can raise their IRMAA tax, two years from now, by as much as $3,470! I.e., an extra dollar of income can be taxed at a 347,000 percent rate! And the subsequent dollar of income? Its additional IRMAA tax is zero!

Finally, if you live in one of the 42 states that taxes income, your effective marginal tax bracket includes marginal state income taxation. California’s top marginal tax rate is currently 13.3 percent. Yes, there is a SALT (state/local income or sales taxes plus property taxes) exemption from your federal income tax. But it’s capped, so not everyone gets to fully deduct their state income taxes.

If you’re living in, say, Texas, which has no income tax, and aren’t yet taking Social Security or Medicare, you may think the above doesn’t apply to you. Not the case. You will, in time, face Social Security benefit and IRMAA taxation. And your optimal course of lifetime Roth conversions needs to take into account everything about your total tax position in every future year.

Roth Conversions Based on Federal Bracket-Filling is Off Base

To summarize, your 1040 tax table, with its nominal federal marginal tax rates, is just one of four key elements in determining your total effective marginal tax rate at each level of federal taxable income. And your total effective marginal tax-rate schedules this year and in future years are, in general, extraordinarily non-linear. Given this non-linearity, trying to optimize Roth conversions by moving taxable income into low federal-bracket years can easily miss the forest for the trees.

The proper approach, which MaxiFi follows, is to search globally over alternative Roth conversion strategies with the proper objective — minimization of lifetime taxes, not filling up poorly defined federal tax brackets.

How Much Roth Tax Savings Will You Sacrifice by Bracket Filling?

The answer depends, of course, on your particular household’s circumstances — demographic and financial. But let me at least illustrate what’s at stake in following Wall Street’s/AI’s Roth advice.

Consider hypothetical John, a single, retired, 62-year-old Oregonian born 6/1/1964. John lives in a $500K paid-off, Oregon house, with $25K in annual expenses. He loves his house and has no plans to sell. He wants to continue fishing off his porch on Lake Oswego through, he hopes, his maximum age of life — age 100.

John has $2 million in regular assets and $2 million in a regular IRA. How did John accumulate so much money? He went to work for his dad’s plumbing company straight out of high school. That age-18 job paid $40K and his nominal salary rose each year thereafter by 3 percent.

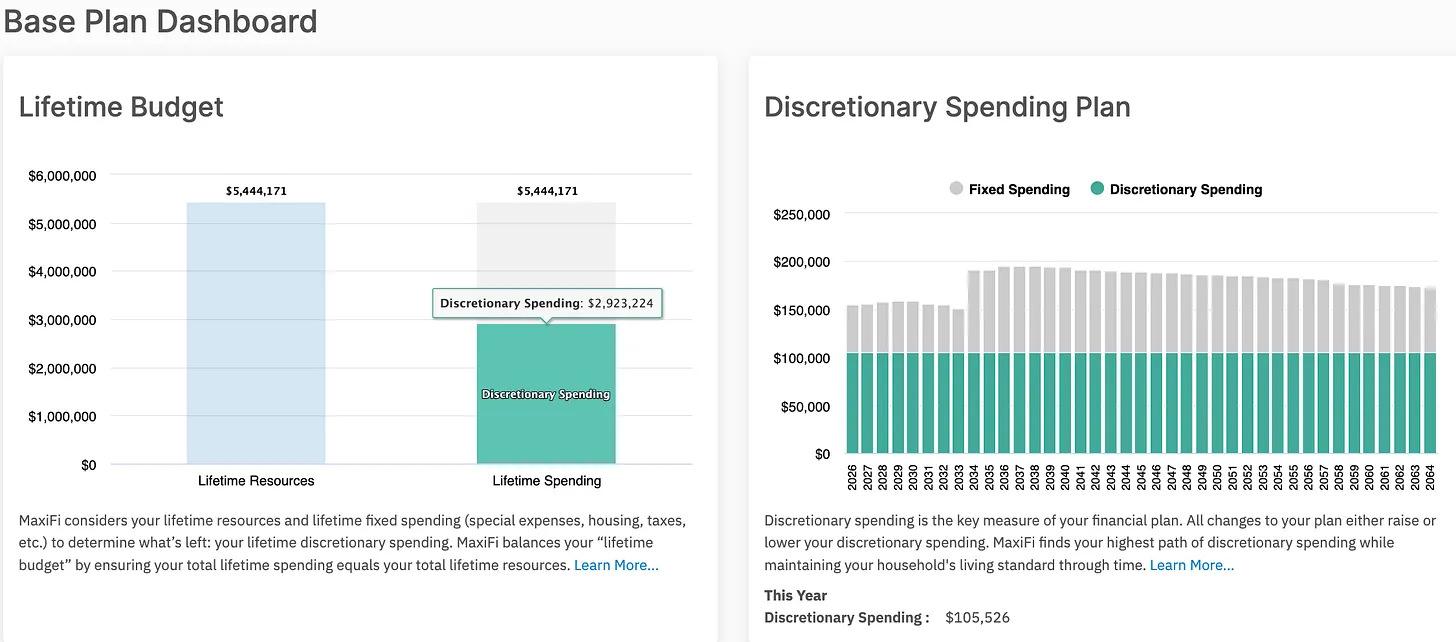

John’s Base Plan

John runs MaxiFi assuming he’ll take Social Security next month when he turns 62, he’ll start smooth IRA withdrawals at 70, inflation will run at 3 percent, he’ll earn 5 percent nominal on his assets, and that federal and state income taxes will permanently rise by 20 percent starting in 2028. (John just read my Substack about America’s extreme fiscal insolvency.)

Here’s results from John’s base plan. John can afford discretionary spending of $105,526 annually measured in today’s dollars. Discretionary spending is spending over and above John’s fixed/required spending on housing and federal and state income taxes, including IRMAA “premiums.”

Optimal and Bracket-Filling Roth Conversions

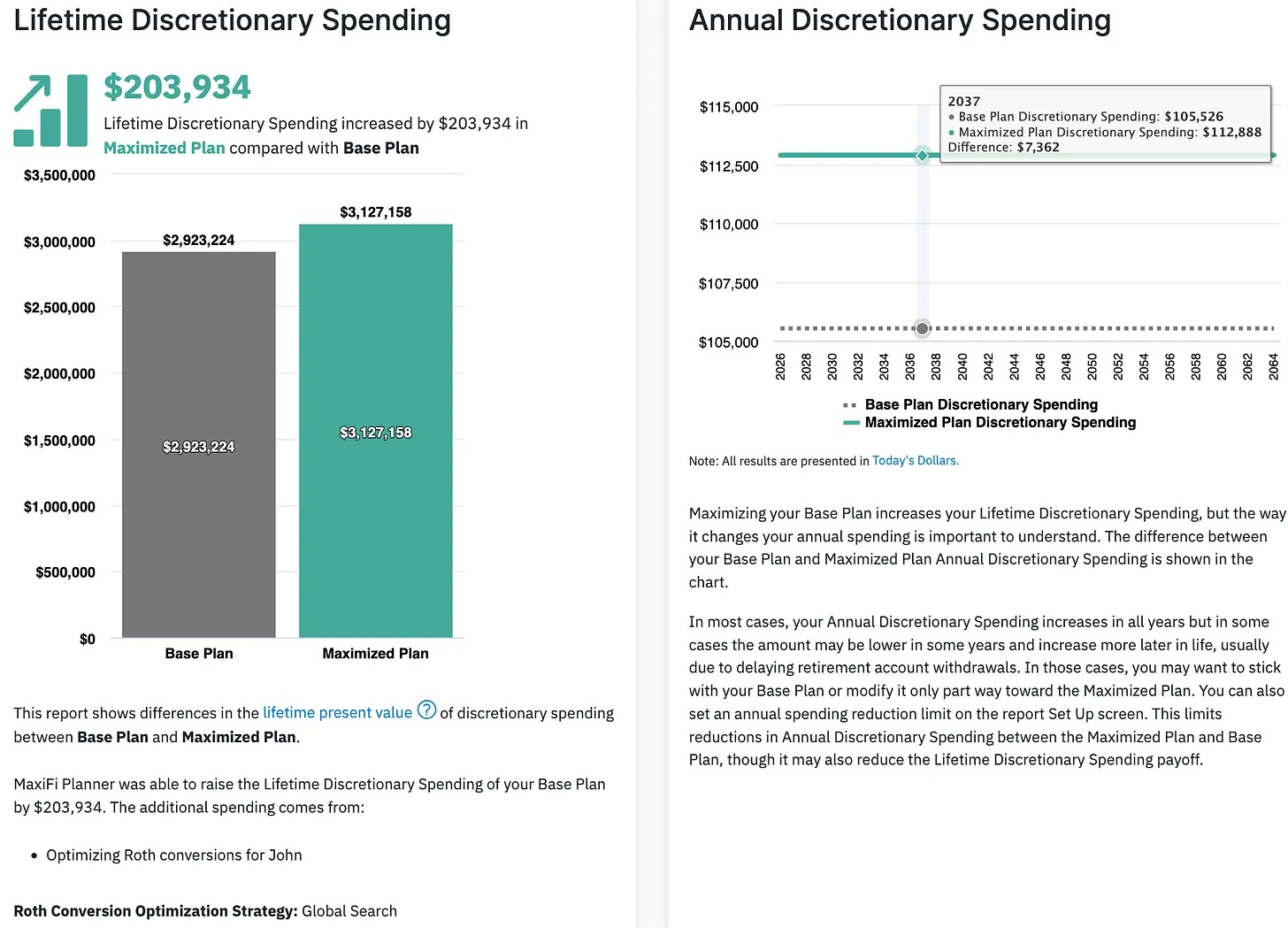

Next John runs MaxiFi’s Roth optimizer and learns he can lower his lifetime taxes and raise his lifetime spending by $203,943. That’s two years of after-tax earnings based on his last year of work! Achieving this optimum entails converting $1,623,280 of his $2 million regular IRA over this year and next. Of the conversion total, $1,293,600 is converted this year and $329,680 is converted next year. This is go big or go home in spades. But it’s no different from taking a very strong antibiotic for a week and watching your infected leg heal versus ignoring the doctor’s orders, taking it a bit at a time over a month and end up … .

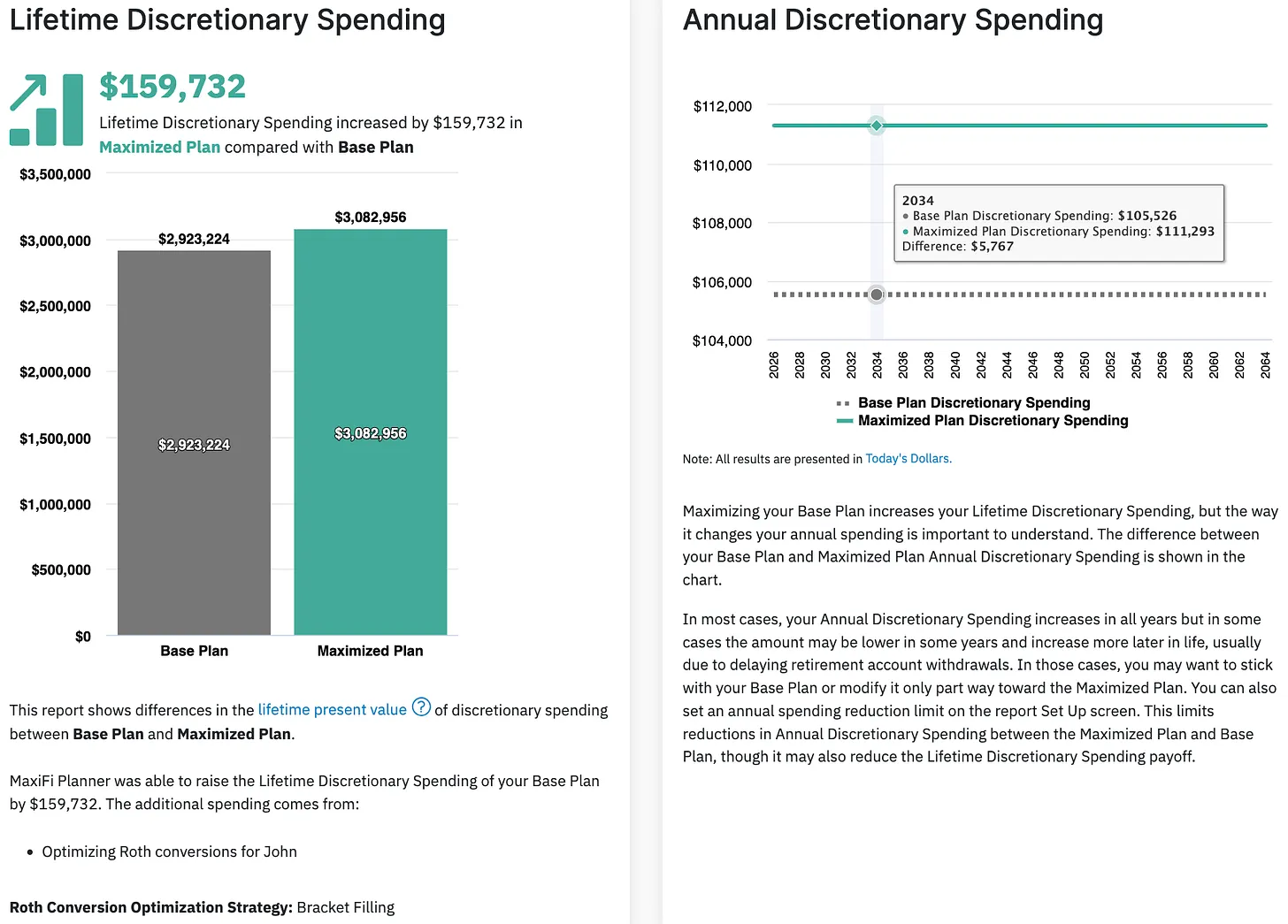

What if John optimally bracket fills rather than follows MaxiFi optimal conversion strategy? The gains are now $159,732 or $44,202 less than the optimal strategy generates. Total conversions are also different — $1,052,500 versus $1,623,280. And John is now told to drag out his conversions by converting roughly $115K over each of the next eight years.

John Optimizes Over Social Security and Roth Conversions

John’s psyched to find more safe money. Next he optimizes over his Social Security collection date. Doing so, assuming no Roth conversions, raises his lifetime discretionary spending by $153,059! MaxiFi’s guidance here is to wait till 70 to start collecting.

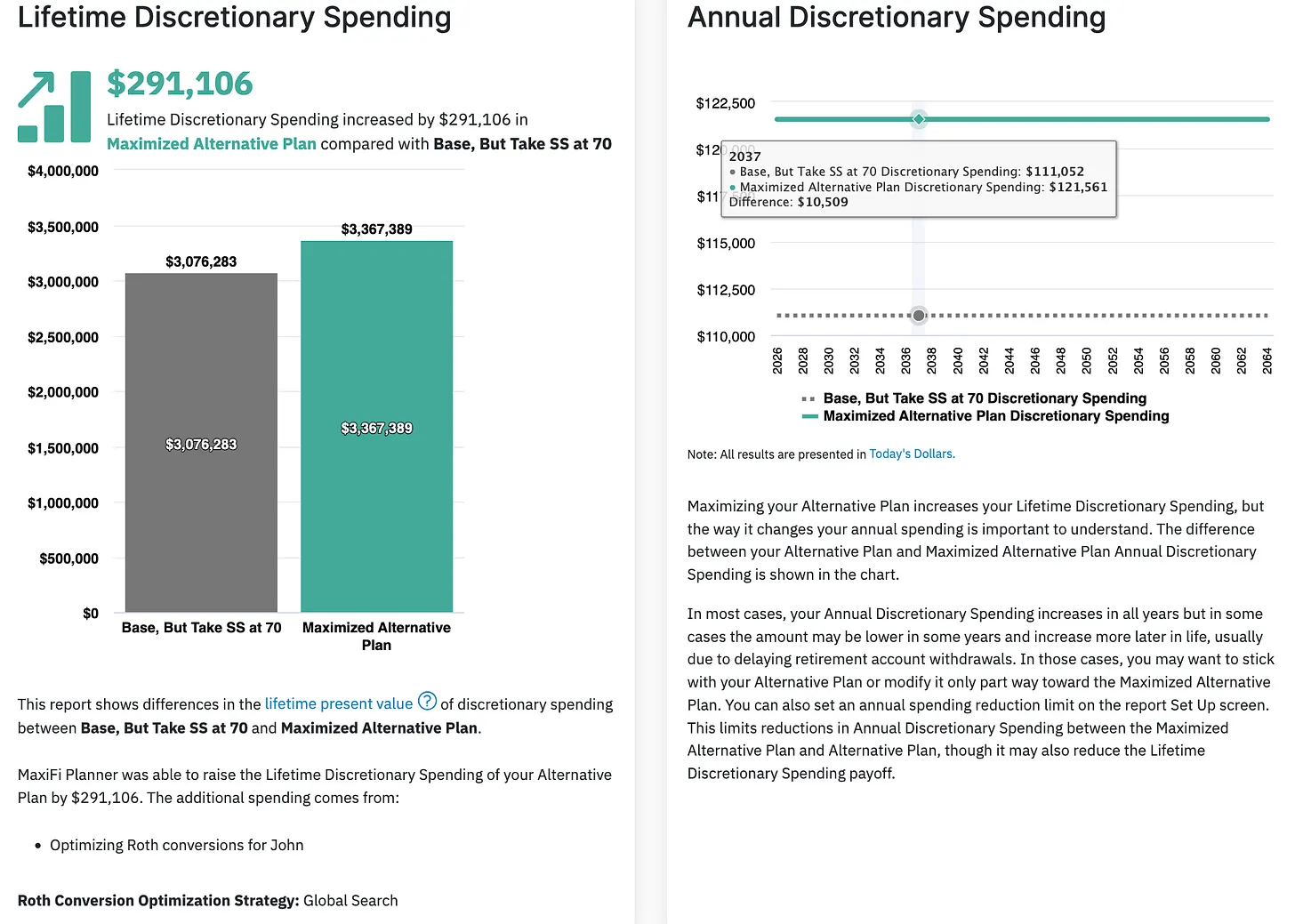

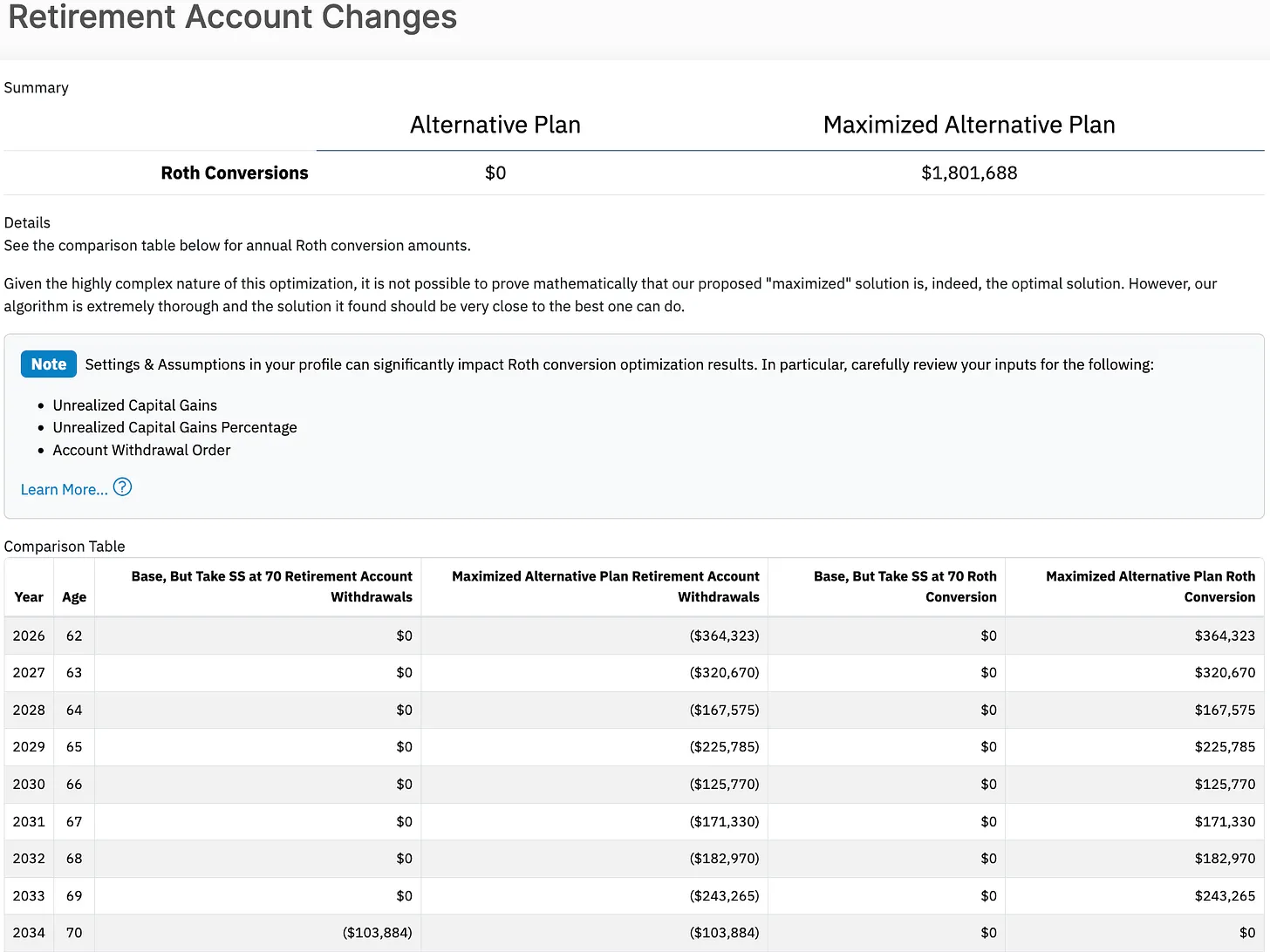

Next, John runs MaxiFi’s Roth Conversion Optimizer assuming Social Security benefit collection at age 70. This produces an extra $291,106 in lifetime tax savings.

The optimal conversion schedule is now very different. John converts almost all of his regular IRA — $1,801,688, but, as indicated, does his conversions more gradually. In waiting till 70 to collect Social Security, he doesn’t need to rush to convert to ensure IRA withdrawals won’t generate high levels of Social Security benefit taxation.

What about bracket filling? How does it do compared with proper global optimization? It reduces John’s lifetime tax savings from $291,106 to $257,729 or by $33,377. That’s not a massive difference. But why, John asks his neighbor, a Wall Street adviser, leave $33K on the table?

MaxiFi’s Joint Optimization — John’s Bottom Line

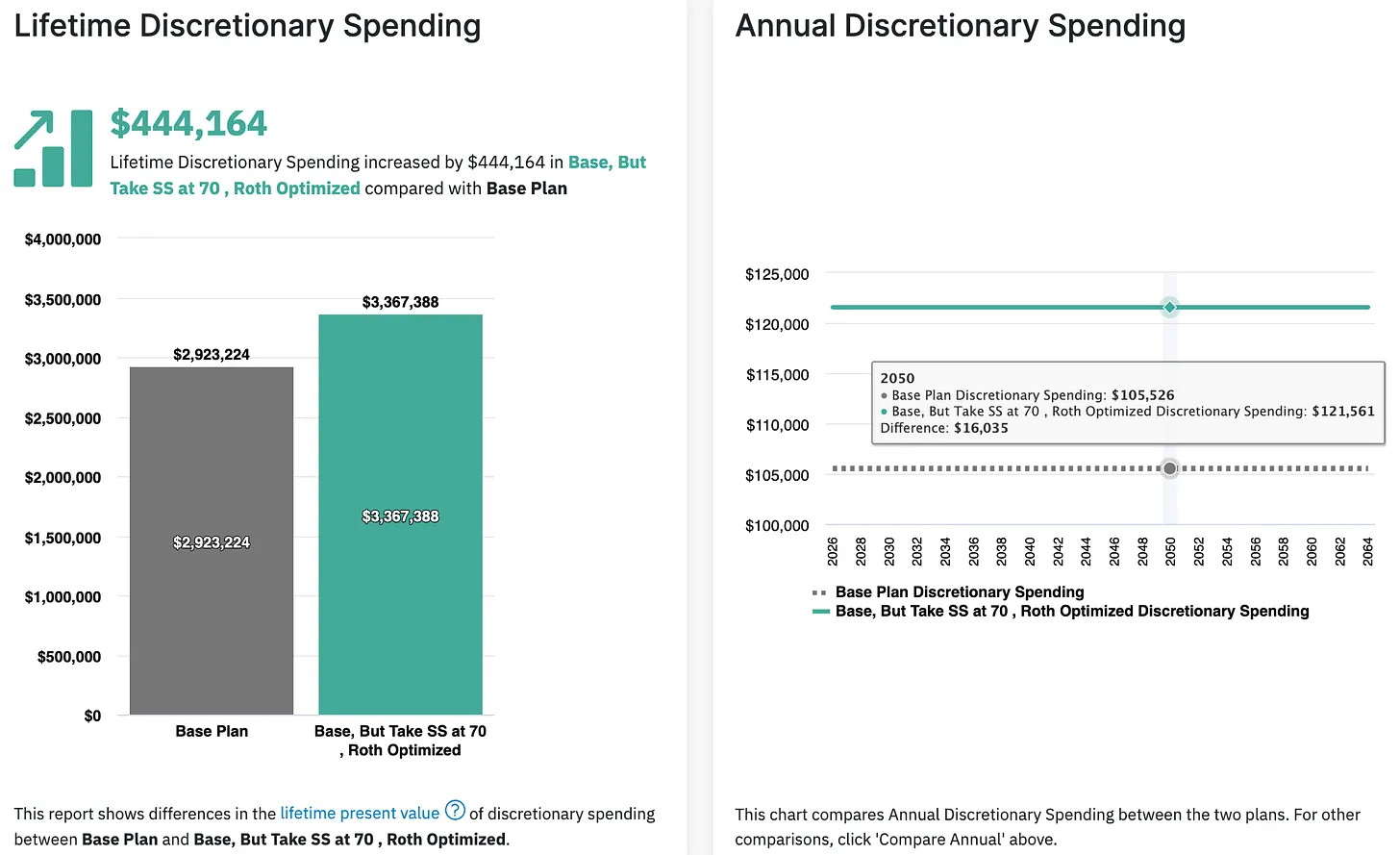

The next chart shows the impact, relative to John’s base plan, of MaxiFi’s jointly optimizing over both Social Security and Roth conversions. The discretionary spending increase/lifetime tax reduction is $444,164 or about four years of John’s pre-retirement after-tax earnings!

Wall Street-Trained Claude Has No Clue

I fed Claude all of the data about John. It concluded that John’s real sustainable discretionary spending was $167,000 per year or 72.7 percent more than John can afford! If John were to spend at that level, he’d run out of money mid-retirement. Claude measures John’s lifetime spending at $692,533, when it’s $3,367,388! Claude does tell John to wait till 70 to take Social Security and Roth convert most of his regular IRA. As for Roth conversions, Claude’s all about bracket filling and inappropriately advises John Roth do essentially all of his conversions this year and next.

My bottom line.

Financial Planning is very serious business. Yes the world is uncertain. But you want precisely correct answers to your personal finance questions — not wildly wrong answers that are seemingly free, but actually will cost you a mint.

Related: Retirement Decisions Powered by AI May Be Leaving Six Figures Behind