There was a time when the 60% stocks/40% bonds portfolio mix was useful and applicable to a broad swath of clients, but that’s a bygone era.

Keeping it real, 40% in bonds, while nice in terms of buffering against equity market volatility, is likely far too much for young clients and in this case, “young” can arguably mean under 50 year old. Still, many investors are hardwired to believe certain things, one of which is that as they age, portfolio risk should be pared. Or they should be heavier in fixed income over equities in retirement.

Indeed, retirement portfolios shouldn’t be littered with overly aggressive segments of the equity. Too few dividend payers or too much small-cap growth exposure are examples of mistakes retirees can’t indulge. In broader terms, some retirees are already committing errors by relying on the prosaic wisdom that they need to drastically reduce equity exposure simply because they’re retired.

Chalk that up as another example of why it pays to work with advisors. With life expectancy elevated, access to defined benefit pensions diminished and Social Security not cutting it for many retirees, clients may need to rely on stocks more than they realize.

Where Clients Are Reluctant, Advisors See Opportunity

A new study from the Center for Retirement Research Boston College sheds light on the retiree equity allocation conundrum. In simple terms, the study reveals older retirees tend to have negative views on stocks and that advisors tend to encourage retired clients with average levels of risk tolerance to increase equity exposure. The latter point might sound someone is being forced to do something they’re uncomfortable with, but the study says clients ultimately benefit.

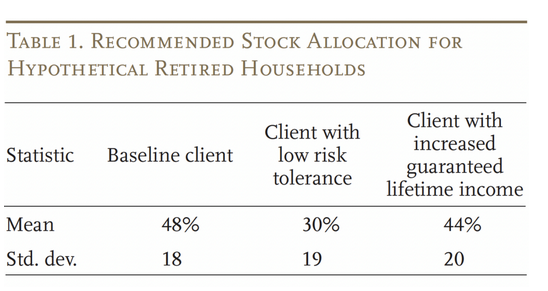

Bear in mind that BC surveyed 400 advisors that have been in the business for at least three years with a minimum of 75 clients and at least $30 million in assets under management. The other requirement was that surveyed advisors had at least 40% of clients age 50 and up. On the investor side of the equation, 1,016 people 48 to 78 with at least $100,000 in assets were polled. As noted in the table below, risk averse retirees likely need some encouragement regarding equity exposure.

(Image: Center for Retirement Research Boston College)

“A closer look at advisors’ recommendations reveals significant variation – the recommended stock allocation for the baseline client has a standard deviation of 18 percentage points,” according to the study. “A shift in equity allocation of this magnitude would have a substantial impact on retirement planning; thus, it is important to understand what factors might explain the wide range of recommendations across advisors for the same client. ”

In other words, there are disparities between what advisors advocate in terms of equity exposure and what many retirees think they should have. An encouraging sign is that “counseling” is taking place and risk-averse retirees aren’t being forced into heavier equity exposure without an explanation as to why.

“The discrepancy between advisors’ recommendations and investors’ desired stock allocations suggests that advisors tend to counsel their clients – at least those with moderate risk tolerance – to increase their stock allocations,” adds BC. “This implication is consistent with the fact that actual stock allocations for investors are much closer to advisors’ recommended allocations than to investors’ desired allocations. ”

Advisors Help in Other Ways

In a perfect world, workers will establish relationships with advisors well in advance of retirement, but the world isn’t perfect. Some investors delay, but it’s never too late and forming an advisor partnership in retirement is better than never doing so. At the very least, those relationships help clients adjust, up or down, risk tolerance.

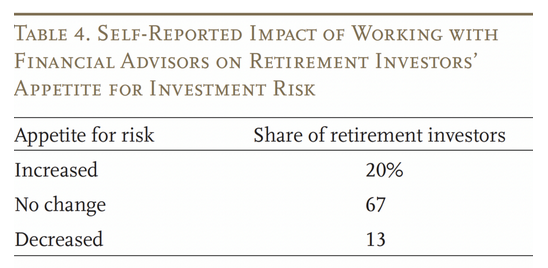

(Image: Center for Retirement Research Boston College)

The above table makes clear that advisors do impact clients’ flair for risk, but not in over-the-top terms. Actually, in the stock/bond debate, advisors are often the more rational party and there’s more to the story and it’s constructive for clients.

“Second, advisors’ average recommendations look quite similar to the stock allocations prescribed by target date funds (TDFs). For example, advisors’ recommended allocations for hypothetical clients with moderate and lower risk tolerance (48 and 30 percent) match the stock allocations of the moderate and conservative variants of the Morningstar Lifetime Allocation Index (48 percent and 32 percent, respectively),” concludes BC.